200 audiobook channels operate in Europe

- 24% of these audio channels are based outside the continent, mainly USA.

- Subscription represents 34% of the total audio entities.

- A-la-carte (unit sale) channels represent 26% of the total audio entities.

- A growing trend is the emergence of audio channels that offer hybrid models: subscription services with optional unit sale purchase represents 18% of the total audio entities.

- Aggregators / distributors represent 10% of the total audio entities.

- Children content devices represent 6% of the total audio entities.

- Library channels represent 6% of the total audio entities.

London, March 11th, 2024. Close to 200 audiobook channels operate in Europe, exactly 192 entities, according to the first “European Audiobook Sales Channels Map” which will be presented on Wednesday March 13th at the London Book Fair by Dosdoce.com, an online platform specialized in analyzing digital trends in the publishing sector, in collaboration with EARS.

From a business perspective, the subscription model is the most popular audiobook channel across Europe representing 34% of the total audio players, closely followed by “A-la-carte” (also known as unit sale downloads) model which represent another 26% of the audio channels identified in the study. A growing trend detected during the research of this study is the emergence of new audiobook commercial players that offer a hybrid model: an unlimited subscription service with optional unit sale purchases. This model represents 18% of the total audio entities operating in Europe.

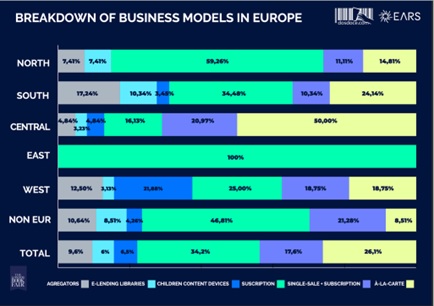

Analysis / breakdown of the audio channel business models by region

The Nordic region is the territory that has the largest offer of subscription platforms representing up to 59% of the audiobook sales channels operating in the region. In contrast, the Central region is the territory that has the largest “A-la-carte” market penetration representing up to 50% of the audiobook sales channels operating in the region. Another trend identified during the research phase of the Map is the growing presence of children content devices across Europe. United Kingdom, France and Beneñux are the countries with the highest penetration of children content devices representing up to 22% of the audio sales channels in these territories.

More and more library users across Europe can enjoy audiobooks across the existing library e-lending platforms, representing 6% of the total audio channels. The South of Europe (Spain, Portugal, Italy and Greece) is the region that offers the largest number of e-lending audio platforms reaching 10% of the total channels, followed UK and France with less than 3%.

Country of origin of the audio channels – Comparative analysis by regions

Central Europe remains the “A-la-carte” fortress.

Central Europe is by far the largest territory (Germany, Austria, Poland, Czech Republic, etc.) embracing audio entities, representing 31% of the existing audiobook sales channels created in Europe. 50% of the players operating in Central Europe have a “A-la-carte” business model, followed by subscription (21%) and hybrid model platforms (16%).

The Nordics have created a subscription paradise.

59% of the players in the Nordics are subscription platforms. “A-la-carte” services represent less than 15% of the total players created in this region.

France, UK and the Benelux offer an interesting equilibrium of business models.

France, UK and the Benelux have created together 16% the existing audiobook sales channels operating in Europe with a very interesting equilibrium between the business models created: 25% of the audio channels in this region are subscription services, closely followed by children content devices representing 22% of the channels created. Unit sales download and the hybrid model represent each 19%.

Southern Europe opts for subscription and library e-lending services.

The Southern European territories (Spain, Portugal, Italy and Greece) have contributed with another 14.5% of the existing audio channel operating in Europe. Subscription is the leading category representing 35% of the total players, followed by “A-la-carte” services (24%) and e-Lending platforms with 10%.

Eastern Europe: a new territory to explore.

Eastern Europe has contributed with less than 1% of the total audio channels.

The USA represents of 80% of the international channels operating in Europe.

24% of the audio platforms operating in Europe are based outside the continent, mainly from the USA, representing 80% of these channels. Non-European audio channels are mainly represented by subscription platforms (47%), followed by those offering the hybrid model (21%); aggregators (11%), then followed by single-unit sale channels and e-lending libraries (each with 8,5%); and children content devices represents only 4% of the total international platers.

Click on this link (PDF) to download the full report.